Selling a luxury property isn’t just about putting it on the MLS and waiting for buyers to appear. These homes occupy a unique segment of the market where expectations are higher, the audience is smaller, and details make all the difference. Working with an agent who understands the nuances of high-end real estate can have a measurable impact on both your experience and your results.

A seasoned luxury agent knows how to position your property to appeal to qualified buyers who appreciate its distinctive features. Professional photography, cinematic video tours, drone footage, and elegant staging are standard tools in their marketing plan, not afterthoughts. They know how to craft the narrative of your home, highlighting architectural design, craftsmanship, and lifestyle elements that set it apart.

In today’s interconnected world, exposure matters. Experienced agents leverage global marketing channels, including luxury-brand websites, international listing networks, and curated print publications. They maintain relationships with agents who specialize in the upper-tier market locally and abroad, extending your property’s reach far beyond traditional advertising.

Equally important is how they handle negotiations. Buyers of luxury homes are often sophisticated investors who expect discretion and precision. A skilled agent can balance firmness with finesse protecting your privacy, guiding pricing strategy with data-driven analysis, and negotiating terms that reflect the true value of your property. Their understanding of high-value financing, appraisal nuances, and inspection standards ensures that once an offer is accepted, the transaction moves forward smoothly.

The same expertise benefits buyers of luxury properties, too. Experienced agents can identify opportunities others might overlook, evaluate comparable properties accurately, and negotiate from a position of strength. They understand what features drive long-term value and how to avoid overpaying in a market where every property is one-of-a-kind.

Whether buying or selling, confidence comes from knowing you have a professional who’s comfortable in the luxury space; someone who understands the expectations, communicates effectively with high-net-worth clients, and has a proven record of success in this exclusive segment of the market.

Luxury isn’t just about price; it’s about expertise, presentation, and trust. When it’s time to make your next move in the high-end market, work with an agent who knows how to deliver both the experience and the results your property deserves.

Even seasoned investors can overlook one of the most valuable tools in their toolbox: a great real estate agent. Sure, you may know how to run numbers, analyze cash flow, and calculate cap rates, but the market is more than just math. A skilled agent is in the field every day, tracking trends, uncovering opportunities, and protecting your investment at every step.

Unlike online tools or out-of-date data, a trusted professional has real-time insight. We know when a property hits the market that’s priced below value. We know which neighborhoods are on the rise, what zoning changes are coming, and how local developments might affect future prices. That kind of information doesn’t show up in a spreadsheet, but it can make all the difference.

We’re also here when timing matters. Because we’re in the market every day, we can spot spur-of-the-moment deals you might miss. Whether it’s a motivated seller, a pocket listing, or a rental-ready property with great ROI potential, our eyes are always open.

When it comes time to make an offer, we do more than fill in the blanks. We negotiate strategically, navigate inspection issues, and help structure the sale to protect your bottom line. And our network of contractors, lenders, inspectors, and property managers saves you time and costly mistakes.

And let’s not forget, real estate laws and contract timelines aren’t always straightforward. We make sure everything is handled professionally and in compliance, so you can focus on the big picture…building long-term wealth.

Real estate investment is part numbers, part strategy, and all about who you trust to guide you. If you’re thinking about investing or want a second opinion on a property, reach out. We’d love to help you identify your next opportunity.

If you’ve been sitting on the sidelines waiting for mortgage rates to drop, you may want to reconsider. Rates are already below their long-term average, and every month of delay could mean missing out on equity growth through appreciation and loan paydown. Here’s why acting now may be smarter than waiting.

According to Freddie Mac’s Primary Mortgage Market Survey, the 60-year average for 30-year mortgages is about 7.7%. Today’s rates, around 6.25%, are already well below that historical benchmark. While many people remember the record-low COVID rates near 3%, it’s unlikely we’ll see those conditions again soon.

The Cost of Waiting

Let’s say you purchase a $400,000 home today with a 30-year mortgage at 6.25%. Your monthly principal and interest would be about $2,462.

With average appreciation at 4% per year, after five years your home could be worth about $486,600…that’s an equity gain of nearly $87,000 just from appreciation. Add another $40,000…$45,000 from paying down your mortgage (amortization), and you’ve built more than $125,000 in equity in just five years.

Now, compare that to waiting:

The same home could cost significantly more in five years.

You miss out on years of appreciation and amortization.

If rates dip, more buyers will rush in, driving up competition and prices.

A Smarter Play

The better strategy is to buy now, start building equity, and refinance later if rates go down. This way, you secure today’s price and immediately benefit from appreciation and amortization without risking being priced out of the market.

Waiting for the “perfect” rate is like waiting for lightning to strike twice. With today’s rates still below the long-term average, the real risk isn’t paying too much in interest; it’s missing out on years of wealth-building opportunity through homeownership.

Real estate decisions are among the most significant financial moves a person can make, and the process can often feel overwhelming. That’s why trust isn’t just helpful…it’s essential. The agent you work with should demonstrate unwavering professionalism, honest communication, and a commitment to your best interests at every step.

When trust is in place, everything else becomes easier. Questions are welcomed, advice feels sincere, and decisions are made with confidence. Buying or selling a home becomes less about stress and more about progress.

A Reliable Guide Through Complex Terrain

Real estate isn’t just about numbers and contracts; it’s about people. And having a dependable professional by your side ensures that you’re not facing the process alone. A trusted advisor brings insight, empathy, and experience that can help you weigh options, overcome obstacles, and avoid costly mistakes.

Clear Communication, Better Outcomes

Misunderstandings in real estate can lead to missed opportunities or unnecessary stress. Consistent, transparent communication is how we make sure you always know what’s happening and why. From the initial consultation through closing day, we’re here to clarify the details and provide guidance you can trust.

Built for the Long Haul

The best agents aren’t just trying to close a deal; they’re building relationships that last. When trust is earned, it turns one successful transaction into a lifetime of opportunities, referrals, and peace of mind. Long after the paperwork is signed, your agent should be someone you feel comfortable turning to for real estate questions, resources, and updates.

Knowledge That Works in Your Favor

Trust is strengthened by expertise. Whether it’s understanding local market conditions, evaluating offers, or navigating regulations, a seasoned professional brings tools and insights that help you move forward with clarity and confidence.

Problem-Solving You Can Rely On

Every real estate transaction has its hurdles. Whether it’s a home inspection issue, financing snag, or negotiating point, having a steady hand guiding the way can make all the difference. A trustworthy advisor approaches challenges with calm, creativity, and persistence—always looking for the win-win solution.

Let’s Build Something Great Together

Whether you’re thinking about buying, selling, or just exploring your options, we’re here to offer guidance backed by integrity, experience, and trust. Let’s connect and see how we can help you make your next move with confidence.

As we start 2026, homeowners may have questions about their home, the local market, and what changes, if any, might make sense down the road. Even if moving isn’t on your radar, your home is still one of your biggest assets, and staying informed can help you make better decisions over time.

That’s why we offer a service called Homeowner Advisory.

Homeowner Advisory is a complimentary, no-pressure resource designed to help homeowners get answers, clarity, and guidance about their home and the real estate market, whether plans involve moving soon, years from now, or not at all. It’s meant to be a place you can turn when questions come up, without feeling like you’re starting a sales conversation.

Use the Homeowner Advisory to talk through things like:

Your home’s current value and how it has changed

Local market conditions and trends

Which improvements typically offer the best return

Property taxes or assessment questions

Maintenance planning or finding reliable service providers

Refinancing, equity, or long-term financial considerations

Rental properties, second homes, or future lifestyle ideas

Every Advisory includes a basic overview of your home’s current value so the conversation is grounded in real information, not guesswork. From there, the discussion follows what you want to understand or explore.

Just as important is what Homeowner Advisory isn’t. It’s not a listing presentation. It’s not a sales pitch. And, it’s not tied to timing or obligation.

There’s no expectation to buy or sell, and no pressure to make decisions. The goal is simply to help you stay informed and confident about your home and the market around it.

My role is to be a source of real estate information for you, not just when you’re buying or selling, but all the years in between. Questions don’t only come up at transaction time, and you shouldn’t have to wait until then to get reliable answers.

I’ll share more details about Homeowner Advisory later this year for anyone who would like to take advantage of it. For now, just know that it’s available as a resource whenever questions arise.

Staying informed today often makes tomorrow’s decisions easier and I’m always here to help with that. Give me a call at (612) 386-7027 and we’ll arrange a meeting.

When it comes to real estate, one of the most useful tools for understanding market conditions is something called the absorption rate. Simply put, the absorption rate measures how quickly homes are selling in a specific market. It’s calculated by dividing the number of homes sold in a given period by the number of homes currently on the market. This figure gives us a “speedometer” for the market—how fast or slow homes are moving.

In a balanced market, the absorption rate usually reflects about five to six months of inventory. That means if no new homes were listed, it would take five to six months to sell all the homes currently available at the existing sales pace. When the absorption rate dips below five months, we enter seller’s market conditions. This signals high demand and low inventory, which often leads to faster sales, competitive bidding, and multiple offers. On the other hand, when the absorption rate climbs above six months, it indicates a buyer’s market. Homes take longer to sell, inventory grows, and buyers often gain leverage in negotiations.

The absorption rate also plays a big role in setting strategy. In a high-absorption market, where demand is strong, pricing a home aggressively and preparing for a fast sale can make sense. In a low-absorption market, pricing more competitively and offering buyer incentives may be the best way to attract attention. Sellers benefit from knowing these dynamics upfront, because it helps them set realistic expectations about how long their home might take to sell and whether adjustments to price or presentation may be necessary.

It’s also important to remember that real estate is local. While you may hear national statistics on the housing market, the absorption rate is most useful when applied to your local area—even down to specific neighborhoods or price ranges. That’s because each market has its own rhythm, and broad averages rarely capture the nuances of your community.

Think of absorption rate as a snapshot of market velocity. Just like traffic speed tells you whether the road is clear or congested, absorption rate tells buyers and sellers whether the market is moving quickly or slowly. Armed with this knowledge, you can make more informed decisions, whether you’re preparing to buy, sell, or simply stay up to date with your neighborhood’s market activity.

If you have questions, or if I can help, please give me a call at (612) 386-7027.

When it comes to buying or selling a home, most of us expect a familiar process: offer, contract, closing. But starting December 1, 2025, a new federal regulation could change what’s required in certain transactions… and we want you to be informed ahead of time.

The Financial Crimes Enforcement Network (FinCEN) is launching a nationwide rule that targets residential real estate purchases made by companies, LLCs, or trusts, especially when there’s no traditional mortgage involved (i.e., an all-cash purchase or funding from a private lender without anti-money laundering safeguards).

While the goal of the rule is to prevent illegal financial activity like money laundering, it could impact legitimate transactions including those involving estate planning, real estate investments, or business-owned property.

What Does This Mean for Homeowners?

If you’re selling a home to a buyer who is using a trust, LLC, or corporation without a bank loan, new reporting requirements may apply.

Buyers may be asked to disclose who truly owns or controls the buying entity — something that wasn’t previously required in many deals.

These rules apply to residential properties, including vacant land intended for housing, single-family homes, condos, and co-ops.

The rule also affects transactions handled by title companies, attorneys, or escrow officers — who may now be required to file new federal reports.

How This Could Affect Your Next Transaction

This change doesn’t affect most typical home sales, especially those involving conventional financing. But if you’re ever involved in a more complex sale — like a cash deal, an investment property held in an LLC, or an inherited home going into a trust — it’s possible that new disclosures or paperwork may be needed.

Don’t worry, we’ll guide you every step of the way. As your trusted real estate professionals, we stay on top of regulatory changes like this so you don’t have to. If these rules apply to your situation, we’ll make sure you understand what’s required and help coordinate with your closing team.

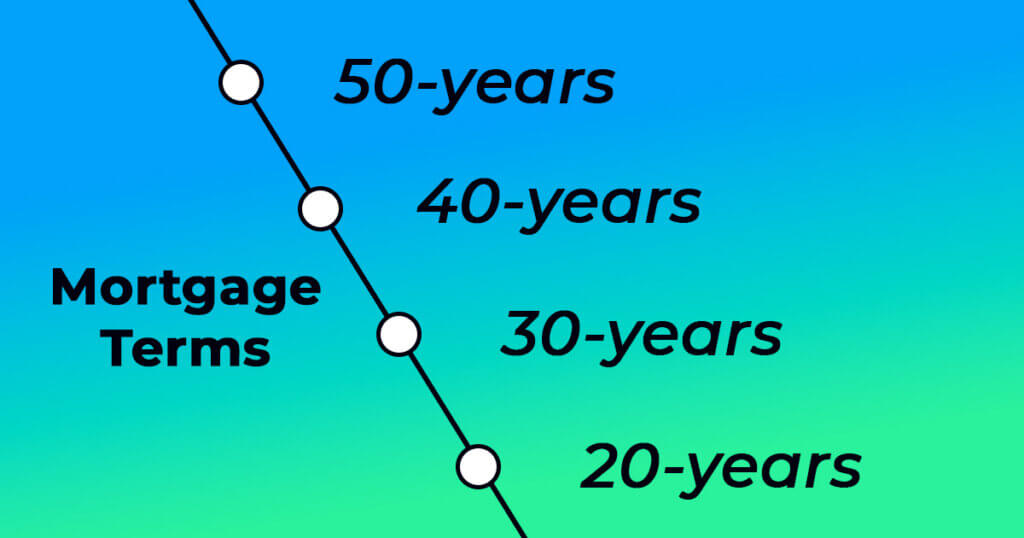

A lower monthly payment sounds appealing but it may come at a much higher price.

When buyers hear about 40 or 50-year mortgages, it’s easy to see the appeal. The payment is smaller, the budget feels easier, and the dream home seems more within reach. But while stretching out a mortgage can make monthly payments more manageable, it also slows the pace of equity growth and dramatically increases the total interest you’ll pay over time.

To show how this plays out, let’s compare a $350,000 loan on a home purchased for $389,000, assuming an average Freddie Mac 30-year rate of 6.22%, a 40-year loan at 6.72%, and a 50-year loan at 7.22%. The table below shows how much you’d owe after 5, 10, and 15 years and how much equity you’d have if the home appreciated at a steady 3% per year.

Mortgage Comparison: The Long View

Term

Rate

Amortization

After 5 Years

After 10 Years

After 15 Years

Total Interest

30yr

6.22%

360 months

Equity: $124,394

Balance: $326,563

Equity: $228,181

Balance: $294,603

Equity: $355,031

Balance: $251,018

$423,347

40yr

6.72%

480 months

Equity: $111,207

Balance: $339,751

Equity: $197,361

Balance: $325,422

Equity: $299,460

Balance: $306,589

$660,015

50yr

7.22%

600 months

Equity: $105,321

Balance: $345,637

Equity: $185,968

Balance: $336,815

Equity: $281,572

Balance: $324,477

$925,402

(Assumes 3% annual appreciation on a $389,000 purchase price & $350,000 original mortgage.)

At first glance, the longer-term loans appear attractive saving roughly $200 to $300 a month compared to a 30-year mortgage. But that smaller payment comes at a cost.

Equity builds much more slowly. After 10 years, the 30-year borrower has nearly $228,000 in equity, while the 50-year borrower has only $186,000, a difference of over $40,000 in wealth.

Interest piles up dramatically. Over the life of the loan, the 50-year mortgage racks up about $925,000 in interest, more than double what you’d pay on a 30-year loan.

Wealth is delayed, not saved. Because your early payments go mostly to interest, it takes much longer to reach the point where your home is truly building financial security.

While a longer-term loan can make a monthly payment look more affordable, it stretches the payoff horizon, slows your path to equity, and significantly increases your total cost of homeownership. For most buyers, a 30-year mortgage strikes a better balance between affordability and wealth-building.

Before choosing your loan term, it’s worth running the numbers and weighing not just what you can afford monthly but how quickly you want to own more of your home.

If you’ve been sitting on the sidelines, waiting for mortgage rates to drop back below 4% before making a move, it’s time for a reality check. While we all loved the historically low rates of 2020 and 2021, those numbers were driven by extraordinary global circumstances, not typical market trends. And expecting them to return any time soon could lead to missed opportunities that may cost you far more in the long run.

During the height of the pandemic, global economic uncertainty prompted aggressive action from the Federal Reserve, which helped drive mortgage rates to record lows. In January 2021, the 30-year fixed rate bottomed out at 2.65%, the lowest in Freddie Mac’s recorded history, which dates back to 1971. But that wasn’t a normal market. It was a response to an emergency.

Looking at the big picture, the average 30-year mortgage rate over the last 60+ years has hovered around 7.74%. Even today’s rates, currently in the mid 6% range, are below that historical average. In other words, we’re not in a high-rate environment; we’re back in a normal one.

The danger in holding out for rates to drop back to those pandemic lows is that the market isn’t standing still. While you’re waiting, home values continue to rise due to ongoing appreciation, and every mortgage payment you’re not making is equity you’re not building. Between market appreciation and amortization (the reduction of loan principal with each payment), today’s buyers are building thousands of dollars in equity every year.

Let’s say home prices rise by just 5% annually, a fairly conservative estimate based on recent years. A $400,000 home could cost $420,000 or more just a year from now. That extra $20,000 increase easily outweighs any potential savings from a slightly lower mortgage rate. And if rates do dip slightly, competition will likely surge leading to bidding wars and driving prices up even more.

So, whether you’re a first-time buyer or looking to move up, the smarter question isn’t “When will rates drop?” …it’s “What will waiting cost me?”

Today’s market offers opportunities, but they won’t last forever. By acting now, you can start building equity, take advantage of current rates while they’re still below the historical norm, and avoid the risk of rising prices and tighter competition. The bottom line: Don’t let yesterday’s rates stop you from building tomorrow’s wealth.

There’s a classic example used in behavioral psychology: the marshmallow test. In this experiment, children were given a choice: eat one marshmallow now, or wait a little while and get two. The lesson? Those who could delay gratification tended to experience greater success later in life.

That same principle applies beautifully to homeownership.

If your ultimate goal is to one day have your home completely paid off, the question becomes: are you willing to make small sacrifices now so you can reap bigger rewards later? Or will you choose comfort and consumption today and carry the financial burden of a mortgage into your retirement years?

Making regular additional principal payments on your mortgage is one of the smartest forms of delayed gratification. It’s not glamorous. It means driving the same car a little longer, skipping that expensive vacation, or resisting the urge to upgrade your lifestyle with every raise. But those steady, disciplined extra payments�say $100 to $200 each month�can shorten your loan by years and save you tens of thousands of dollars in interest.

More importantly, it puts you on track to own your home outright.

Imagine reaching retirement without a house payment. Your monthly expenses drop dramatically, giving you more flexibility and freedom. You may not need as much in retirement savings. You could choose to work less, travel more, or simply breathe easier knowing that no one can take your home from you.

On the flip side, choosing not to delay gratification, maxing out your lifestyle, refinancing to take cash out, or simply making minimum payments, can mean carrying a mortgage into your 60s or 70s. When many people want to slow down and enjoy the fruits of their labor, they’re still stuck paying for yesterday’s choices.

The marshmallow test isn’t just about kids and candy. It’s about life and how we make financial decisions. A little patience now, a little extra toward your mortgage each month, can lead to a lifetime of reward.

So, ask yourself: will you wait for two marshmallows later? Or settle for just one now? The path to a paid-for home starts with the power of delayed gratification. Use our Equity Accelerator calculator to make projections to pay your home off sooner.

All information is dynamic and can change by the respective companies listed herein at ANYTIME. Use this guide as a reference point ONLY. We believe the information herein it is accurate but not guaranteed and may not be current as we are not able to update all information.